Market regulator SEBI recently came out with a draft circular that outlines a set of important proposals for which it seeks suggestions and comments.

Among the 20 proposals listed in the consultation paper, a few are particularly important and may require the attention of investors if they come through in the future.

Broadly, the proposals pertain to starting of additional schemes (with the same existing mandate) subject to certain thresholds being reached and conditions being met, and the launch of new schemes with target maturity involving equity categories. The regulator has also proposed allowing equity and debt category funds to invest the residual portion (the remaining part after complying with specific category/scheme norms) of their portfolios in a wider range of assets.

We broadly look at the proposals and the possible pros and cons if these do come through.

Old schemes, new launches

Many funds, especially from the older asset management companies (AMCs), have grown enormously in size. SEBI has proposed that these AMCs could launch additional schemes in the same categories as the larger funds.

The conditions are that the fund must have an asset under management (AUM) of more than ₹50,000 crore and must have a track record of at least five years. Now this new additional scheme is expected to have a similar investment objective, strategy and asset allocation as the existing fund. No more than two funds can exist in the same category at any point in time.

When the additional fund is rolled out, SEBI has said that the existing fund must be closed for all subscriptions.

The expense ratio is capped at the rate that the existing fund charged when the NFO of the additional scheme is rolled out.

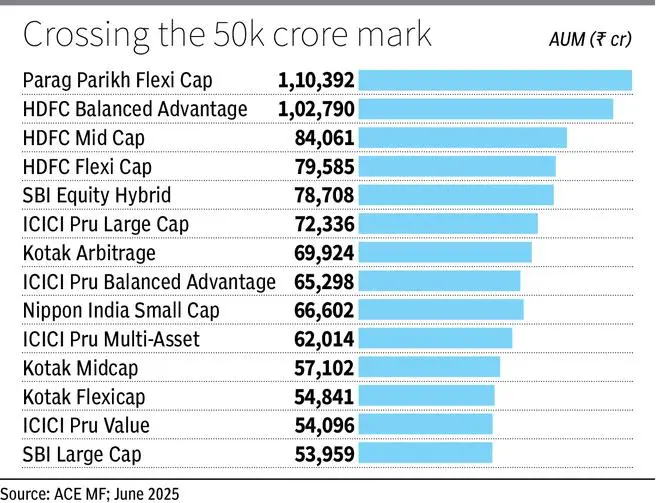

Currently, there are nine equity funds with an asset size of over ₹50,000 crore and five from the hybrid category.

In categories such as mid- and small-caps, this additional fund launch may be of help as a larger AUM is at times seen as a challenge as taking large position in smaller-capitalisation stocks would move the price considerably and increase the impact costs for the fund house.

An additional fund would start from a smaller size and would perhaps be easier to manage.

Besides, it would avoid situations where equity funds sit on huge amounts of cash (more than 25 per cent in some cases) without being able to suitably deploy them.

However, stopping subscription in the existing fund will mean that investors with SIPs running or those prone to deploying periodic lumpsums will have to stop them and instead park the money in the additional scheme, assuming they wish for similar exposure.

If a different fund manager is appointed for the additional scheme and it underperforms, those who shifted SIPs would lose out on returns.

Beside the existing scheme could face redemption pressure, and affect performance.

Overall, this proposal seems a mixed bag.

Value and contra allowed

Currently, AMCs are allowed to have either a value fund or a contra scheme in their offerings.

The market regulator has now made a proposal for allowing fund houses to launch both these schemes. Only one condition has been specified for allowing this move — the portfolio overlap between contra and value schemes of a fund house should not exceed 50 per cent.

Right now, there are just three contra funds and 21 value schemes.

In theory, there is a difference between contrarian and value investing in that the former involves buying out-of-favour stocks, while the latter generally considers undervalued assets relative to their fair value. However, in practice, contra style generally morphs into value investing for most parts. And out-of-favour stocks may also present value opportunities.

Given the mandate of not having an overlap, this proposal gives investors more choices.

Solution-oriented fund for life goals

There are mutual funds now that cater exclusively for the retirement goal with multiple options across equity, hybrid and debt categories.

SEBI has now asked for comments stating whether fund of funds (FoF) could be offered for various goals such as marriage, house purchase and the like, in addition to retirement.

However, there are a few interesting proposals here. It has asked if AMCs should launch FoF with a specific tenure as part of goal planning investment.

These FoFs are proposed for all three categories – equity, hybrid and debt.

Equity FoF would invest in a mix of equity funds of the AMC. For example, the equity FoF could be a combination of the large-, flexi- and mid-cap funds of the house.

However, some conditions are imposed for the hybrid and debt FOFs. Life Cycle FoFs may invest in underlying debt category schemes except for All Seasons Bond category. In the hybrid category, schemes are not allowed to invest in Aggressive Hybrid Fund, Dynamic Asset Allocation, Multi Asset Allocation Fund.

Like target maturity funds, these lifecycle schemes would be operational for a specific timeline and at the end of it, the proceeds would be distributed to unitholders.

How this would work is best described by the regulator’s presentation of a set of options specifically for retirement.

Lifecycle Retirement FoFs are proposed for periods ranging from 10 years to 30 years, in steps of five years.

The retirement Life Cycle FoF 2035 (would mature in 2035), with a tenure of 10 years, will invest in equity funds for the first four years, hybrid funds for the next three years and debt funds for the last three years.

A minimum lock-in period of five years has been suggested.

The retirement Life Cycle FoF 2055 (would mature in 2055), with a tenure of 30 years, will invest in equity funds for the first 24 years, hybrid funds for the next three years and debt funds for the last three years.

While these lifecycle FoFs with lock-in would help remain invested for longer periods and enjoy the benefit of compounding, there are some points of concern.

If there is prolonged underperformance in the underlying funds, exiting schemes may either not be possible or could come with hefty exit loads.

Next, the idea of investing in hybrid funds and debt schemes for the last six years risks huge opportunity loss. Exiting equity funds a year or two before specific goals is fine, but a six-year period of modest returns could result in an insufficient corpus accumulation.

Even in the hybrid funds, three prominent categories are not allowed for investments, leaving only conservative and balanced hybrid funds, which invest modestly in equity (we aren’t considering arbitrage or equity savings funds as their mandates are different).

An NPS-like structure could perhaps work better here with specific allocations to equity and debt funds in keeping with the investor’s age.

Residual investments in REITs and InvITs

The regulator has proposed that mutual funds be allowed to invest the residual portion of their equity category schemes in debt (including money market instruments), gold, silver REITs and InvITs.

For the debt category, SEBI has proposed investment of residual portion in REITs and InvITs. This would, however, not be allowed in overnight, liquid, ultra-short duration, low duration and money market funds.

In the case of hybrid funds, too, it has proposed investing in REITs and InvITs, except for dynamic asset allocation and arbitrage funds.

While these additions broaden the diversification angle of portfolios, it could make assessments of performance difficult, For example, if an equity fund (say flexi-cap) invests in gold, silver, REITs and InvITs etc. to the tune of 20 per cent of its portfolio, it would resemble a multi-asset fund.

Published on July 26, 2025